Modern Home Bulgaria's analysis of banking policies, energy classes and the forecast for the real estate market until 2030.

Mortgage Financing 2026 will be unlike anything we have seen in the last 15 years. While everyone is talking about the euro and prices, a much quieter but equally important change is happening in the banking sector in 2026. The combination of freed up bank capital, new preferential rates for energy-efficient buildings and a growing restriction on the old building stock is reshaping the real estate market in a way that will define transactions for the next 5 years.

In this article we look in detail at:

With Bulgaria's accession to the eurozone on 1 January 2026, the Bulgarian National Bank (BNB) will synchronize its minimum reserve requirements with those of the European Central Bank. In practice, this means that the requirement for banks to hold reserves will drop from 12% to just 1% from the deposit base.

The result is brutally simple: about 16 billion leva of additional liquidity is released, which banks can now lend out instead of keeping frozen in the BNB's vaults.

This is a huge influx of money into the credit market and explains why in the first months of 2026 we see:

For a buyer with a good profile — permanent employment contract, stable income, regular credit analysis — We are at the most favorable time for taking out a mortgage loan in the last 15 years.. Interest rates are low, banks are hungry for customers, and new eurozone regulations are forcing them to be even more aggressive in their supply.

But there is one key caveat— not all properties are equal in the eyes of the bank.

UBB, as part of the Belgian KBC Group, offers Mortgage loan "Energy Efficient Home"„ with a publicly advertised discount 0,15% of the interest rate for properties with energy class A+, A or B and consumption below 150 kWh/m². In combination with the other standard discounts (for salary in the bank, tied products, premium client profile), the real final rate under optimal conditions can reach under 2,30% — one of the lowest levels on the Bulgarian market at the moment.

The typical structure at most leading banks includes:

When all these factors are combined, the actual achievable rate can reach the range 2,20-2,35%. Such a profile usually requires:

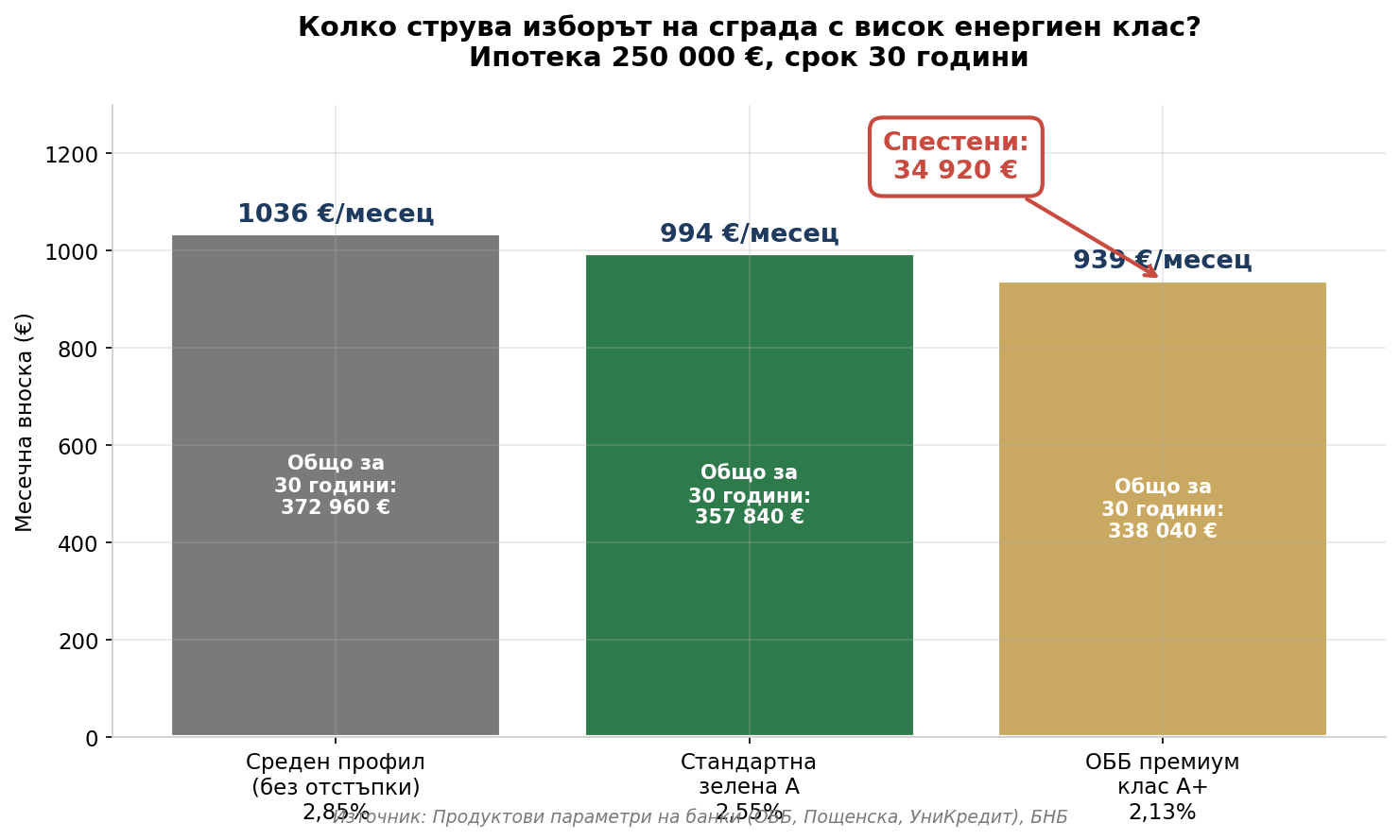

Let's calculate it with a specific example. A mortgage loan of 250,000 euros for 30 years. Important clarification - according to BNB data as of the beginning of 2026. The average interest rate on new housing loans in Bulgaria is 2.46%, which is one of the lowest levels in all of Europe (for comparison, the average in the eurozone is about 3.25%, in Croatia and Germany about 3%). Here are the realistic scenarios:

| Scenario | Interest | Monthly installment | Total paid |

|---|---|---|---|

| Average customer profile (without discounts) | 2,85% | 1 036 € | 372 960 € |

| Green Mortgage Class A (Standard Discount) | 2,55% | 994 € | 357 840 € |

| Optimal — premium class A+ | 2,25% | 955 € | 343 800 € |

The difference between the average profile and the lowest achievable rate is almost 29,000 euros over the term of the loan. With a larger loan or a more aggressive interest rate difference (over 1 percentage point), the savings easily exceed 60,000-70,000 euros. This is the price of a second property in the countryside or the money for a child's education. For the same home, simply because it is in a building with the correct energy class.

Other leading banks follow a similar logic:

The energy efficiency certificate is a document that is issued by a licensed appraiser after construction is completed (or after major renovation/renovation) and assigns the building to one of 7 classes — from A+ (most efficient) to G (worst).

The certificate estimates the annual primary energy consumption per square meter (kWh/m²/year) for:

| Class | Consumption (kWh/m²/year) | Characteristics |

|---|---|---|

| A+ | < 30 | Passive buildings, zero consumption |

| A | 30 – 50 | Highly efficient, new after 2020. |

| B | 50 – 95 | Good modern buildings |

| C | 95 – 150 | Moderately effective |

| D | 150 – 250 | Old, unsanitary |

| E | 250 – 400 | Panel, unrenovated |

| F | 400 – 600 | Highly depreciated |

| G | > 600 | Critically ineffective |

All banks offering „green” interest rates require — in addition to a formal class A or B — a mandatory threshold below 150 kWh/m²/year. per completed project. This excludes many buildings that are nominally class B but actually exceed consumption.

With the accession to the eurozone and the transposition of the updated Directive (EU) 2024/1275 on the Energy Performance of Buildings (EPBD IV), new requirements are introduced:

For buyers, this means that the energy class of a property is no longer just a nice extra — it is a central factor in determining the sales value, access to financing, and liquidity of the property upon resale.

The data here is uncompromising:

Banks respond to this risk in three ways:

1. Reduced financing (LTV). Tokuda Bank is an example — up to 85% of the market value for monolithic construction, but only 75% for panel. In other words, for the same apartment, the buyer must subtract 10% more self-participation out of pocket if the building is paneled.

2. Tying the loan term to the building's service life. If the bank's technical assessment shows that the building has 15 years of remaining service life, the loan cannot be drawn for 30 years. This directly reduces purchasing power.

3. Complete refusal of funding. Some banks no longer accept panel properties as collateral, especially for buildings without renovation and without an up-to-date technical passport.

This creates a downward spiral for owners of prefabricated homes:

Important clarification — it's not just pressure-treated panel construction. The old brick stock (buildings from the 60s to the 90s, before 2005) is also starting to lose competitiveness because:

The only exception is when the owner has carried out a complete renovation with a transition to class B or higher — then the property can receive a green interest upon resale.

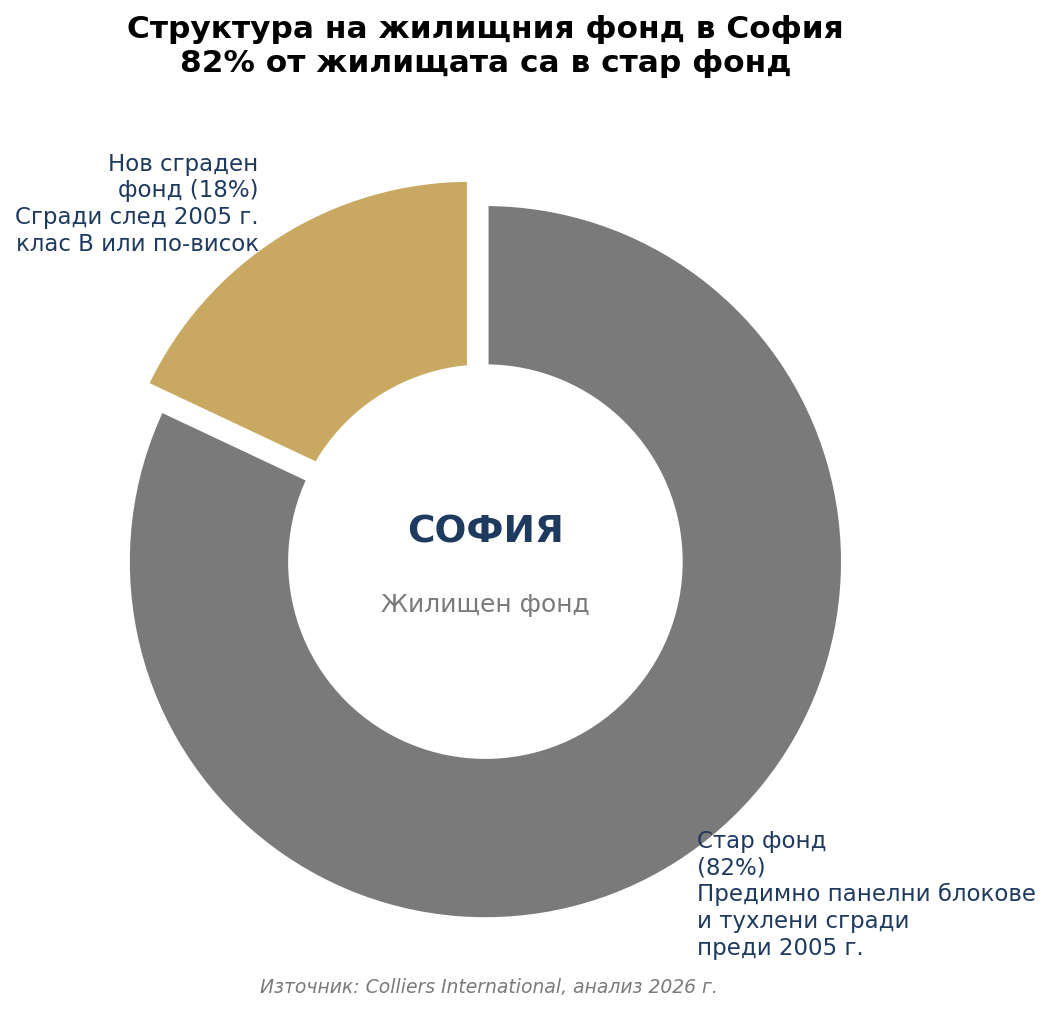

Data from Colliers' latest analysis, presented at the Imoti.net forum in February 2026, shows a worrying picture:

82% of the total housing stock in Sofia is old stock — mostly panel blocks with very small units.

This means that only 18% of the available housing supply in the capital meets modern standards for energy efficiency, modern communications, parking spaces and common areas.

According to NSI data:

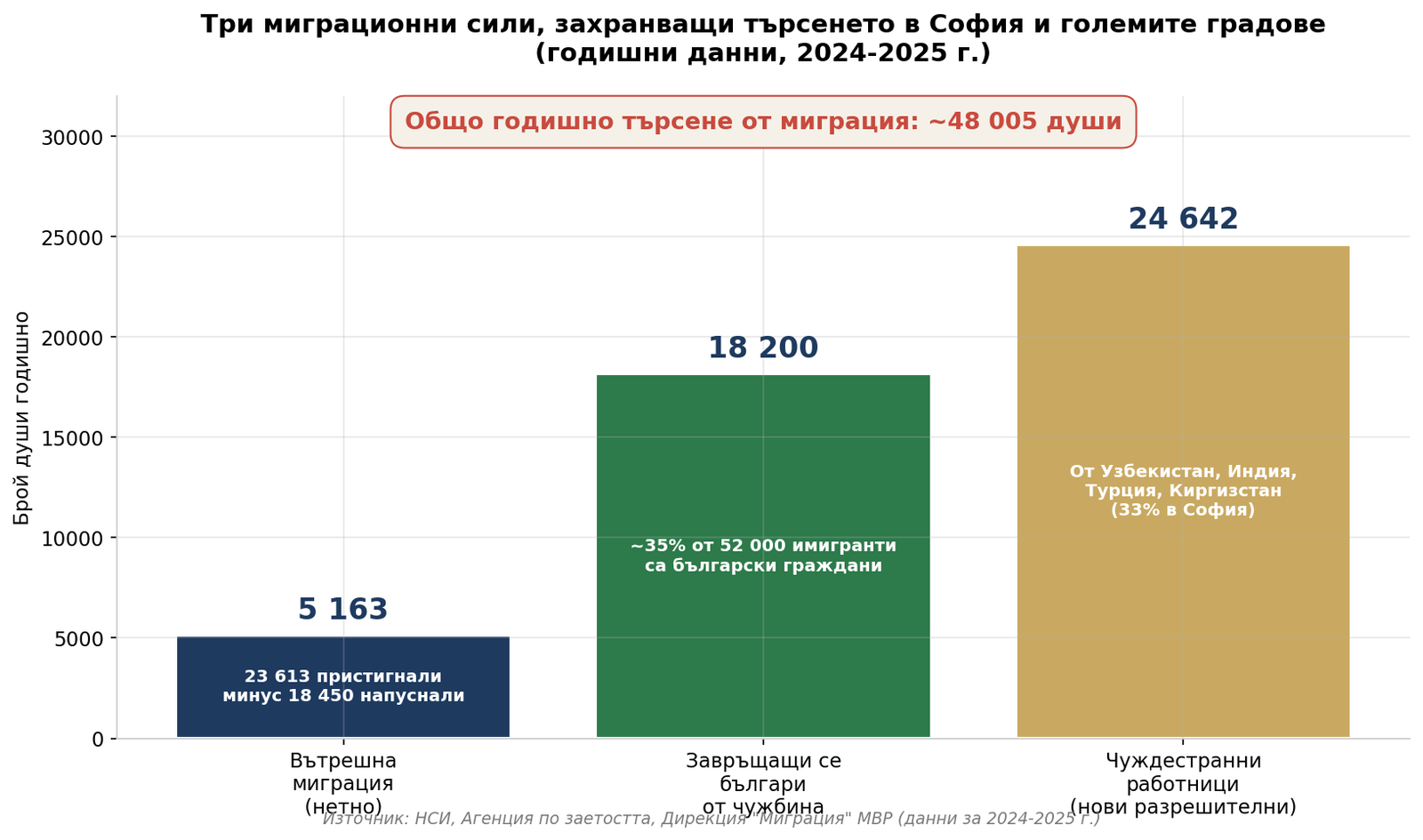

It is important to clarify an often quoted thesis. According to NSI data for 2024, Sofia has settled 23,613 people, but they left it 18 450 — a net increase of about 5,163 people (or 17,000-18,000 people gross according to Colliers estimates). With an average Bulgarian household size of 2.2 people, this means about 8,000 new households per year from internal migration. Against this supply of ~11,000 new homes = potential surplus of ~3,000 homes per year.

This is precisely what Colliers noted as „a reversal of the trend for the first time in 8 years.”. There was a deficit until 2024, and in 2025, a local surplus appears for the first time in the mass segment.

But this picture is incomplete. When we add the other two migratory forces (which we examine in the next section):

| Search source | Annually | Households needed (÷2.2) |

|---|---|---|

| Internal migration in Sofia (gross) | ~18 000 | ~8 000 |

| Returning Bulgarians (out of 18,200, estimated 60% in Sofia) | ~11 000 | ~5 000 |

| Foreign workers in Sofia (33% out of 24,642) | ~8 100 | ~3 500 |

| Total search in Sofia | ~37,000 people | ~16,500 households |

Against these ~16,500 households, only ~11,000 homes are being produced → the real deficit is ~5,500 homes per year in Sofia. The so-called „oversupply” is a local phenomenon — in certain peripheral neighborhoods with mass construction (Vitosha, Manastirski Livadi, parts of Krastova Vada), where the local supply overtakes the local search for a first home.

This is a classic example of how aggregate statistics can be misleading — the market is both in surplus (in certain sub-segments) and in deficit (as a whole).

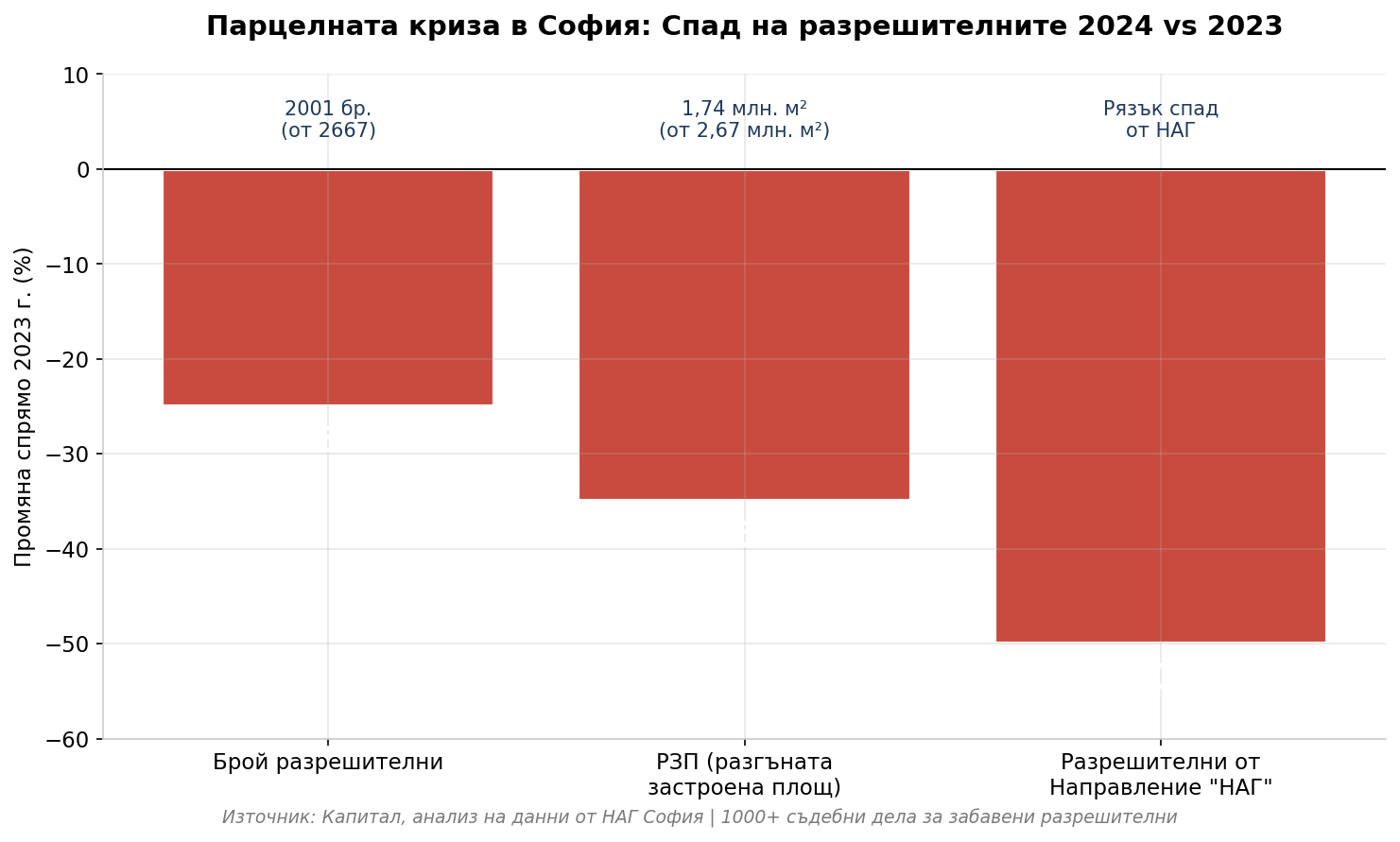

The oversupply we are currently seeing is the result of permits issued in 2021-2023 and now materializing as buildings. But the line behind is already significantly thinner. In 2024, Sofia saw a dramatic contraction of the construction pipeline:

What is behind this:

1. Shortage of built-up plots. Sofia investors already bought up most of the quality plots in established neighborhoods. What remains is either too expensive, has problematic status, or requires complex PUP procedures.

2. The price of land. According to current data 30-40% of the cost of new construction in Sofia is already formed by the price of the plot. When land becomes half the product, the economics of the project become increasingly difficult.

3. Blocked OOP. The general development plan of Sofia dates back to 2007 and is morally outdated. The new one cannot be passed due to complex coordination procedures, which keeps many investment projects in a "gray zone".

4. Overdevelopment and public pressure. The new municipal administration has declared a policy against overdevelopment. Even in the absence of legal grounds for refusal, procedures are significantly delayed, which increases the financial uncertainty of investors.

This dynamic creates a curious paradox for 2026-2027:

This is an important distinction— any price correction will not be deep and will not be long-term. It will be a pause, not a brake.

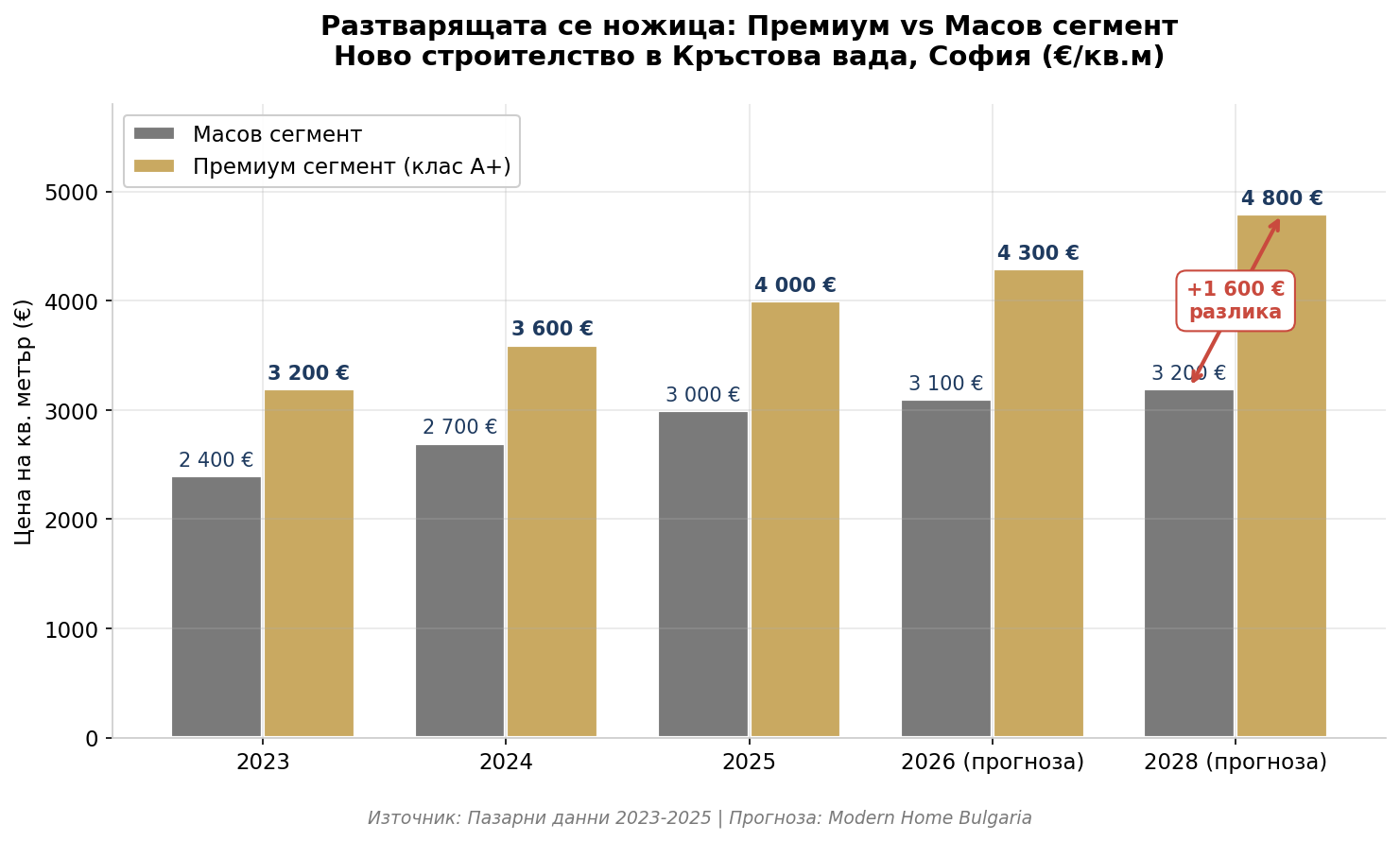

A key obstacle in the oft-repeated thesis of „cooling the market” is that it treats new construction as a homogeneous product. In practice, this is not the case. Even in neighborhoods with oversupply (Vitosha, Krastova Vada, Malinova Dolina, Manastirski Livadi), there are dramatic difference between the premium and mass segments:

Characteristics that will hold or even increase prices even during a market correction:

These properties continue to increase in price even with a macroeconomic cooling, because demand comes from a different segment of buyers — high income, investment motives, quality of life over price.

The standard new construction that dominates the statistics:

Exactly here Oversupply will hit hardest. In a correction, buyers will have more options, the market will slow down, and prices may stagnate or decline slightly.

According to current market data, the difference between the two segments is already moving within the limits 25-40% per sq. meter. In 2025, in Krastova Vada, standard new construction is sold for €2,800-3,200/sq m, and premium projects from established developers (Artex, AG Capital, Ciela Real Estate and others) reach €3,800-4,500/sq m for the same neighborhood. In Lozenets and Ivan Vazov, premium projects already exceed €5,000-5,500/sq m.

Our forecast for the next 3 years — this difference will grow to 40-55%. Mass new construction will stagnate, while the premium segment will continue to grow. This is a classic example of a „two-speed market”.

Several parallel processes determine what will happen by December:

Prices in Sofia: Growth of 5-10% is expected in new construction, but differentiated. Neighborhoods with active new construction (Vitosha, Krastova Vada, Manastirski Livadi) may see stabilization or a slight decline due to oversupply in the mass segment, but premium properties there will continue to increase in price. Established areas with new class A building stock (Lozenets, Iztok, Ivan Vazov) will continue to grow steadily.

Interest rates: The current average market interest rate is 2,46%. It is expected to remain in this range with a slight increase to 2.60-2.80% towards the end of the year, if the ECB starts a gradual increase. Green loans will remain the most profitable option, and UBB will probably maintain its preferential rate.

Construction costs: Growth of another 15-18% in 2026 due to the increase in the price of materials and labor after the euro. This, combined with the shortage of new permits, will support new construction prices from below.

The deals: Moderate decline in volume compared to the „panic” 2024-2025, but better quality deals. Investment purchases (for rental purposes) will decrease significantly — from about 40% of deals to 20-25%.

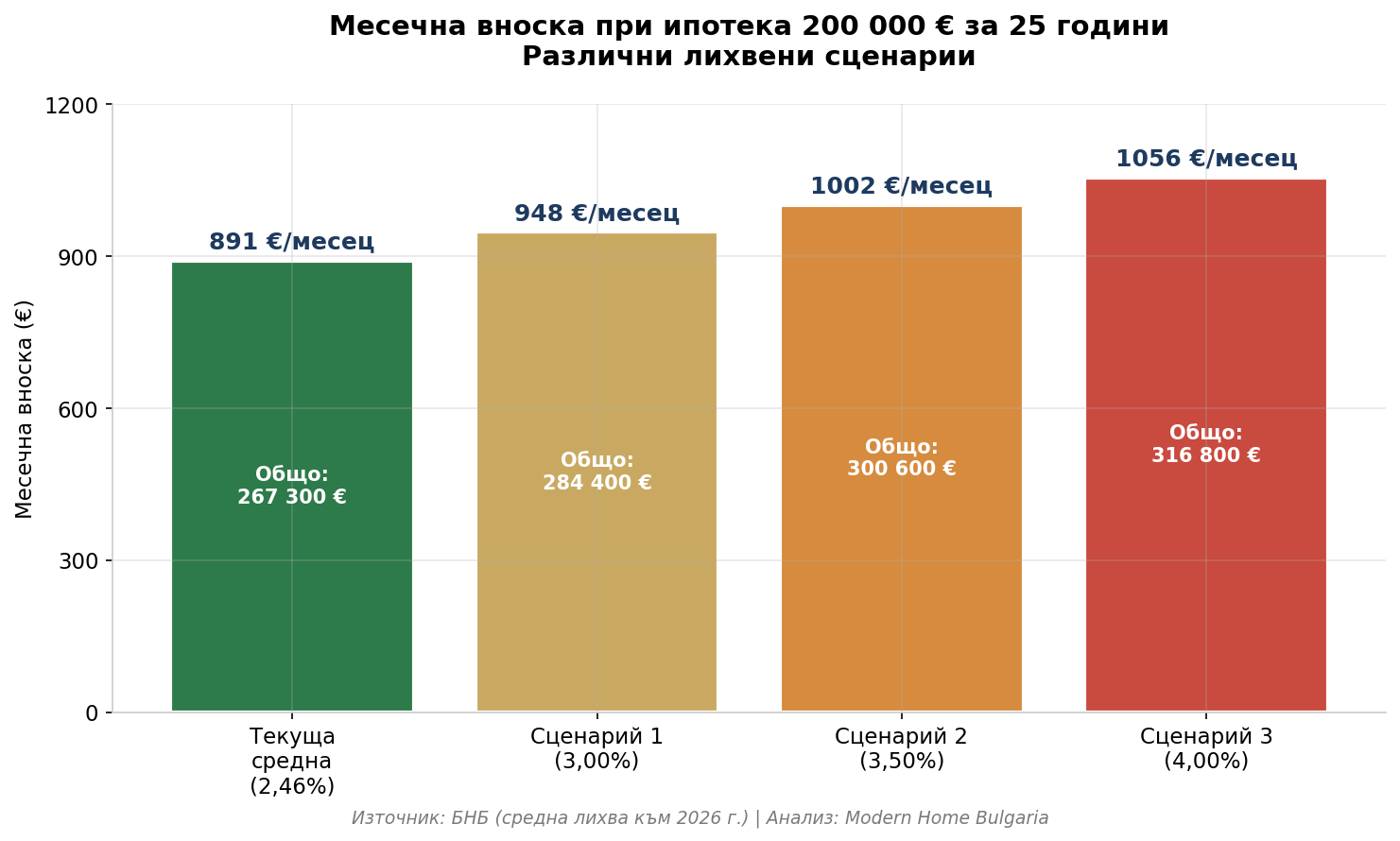

One of the most common fears among buyers right now is: „What if interest rates go up?” Let’s consider a scenario where the average interest rate rises from the current 2.46% to 3,0-4,0% in 2027-2028.

For a mortgage loan of 200,000 euros for 25 years:

| Interest | Monthly installment | Difference vs baseline (2,46%) | Total paid for the term |

|---|---|---|---|

| 2.46% (current average) | 891 € | — | 267 300 € |

| 3,00% | 948 € | +57 € (+6,4%) | 284 400 € |

| 3,50% | 1 002 € | +111 € (+12,5%) | 300 600 € |

| 4,00% | 1 056 € | +165 € (+18,5%) | 316 800 € |

For an average family, this means +57 to +165 euros per month additional payment on the same loan. Sensitive, but far from fatal.

1. Moderate slowdown in demand (-10 to -20% transaction volume). Some of the borderline buyers — people who have difficulty qualifying for credit even today — will drop out. This cools the market, but does not stop it. The historical parallel is clear — in 2022-2023, interest rates in Germany and Italy rose from below 1% to 4-4.5%, but deals there fell by 25-30%, they did not collapse.

2. Adjustment in prices of the mass segment (-5 to -10%). It is the massive new construction we discussed above that will feel the pressure first. This is the segment with the greatest oversupply and the most sensitive to lending. The correction is not a catastrophe — it is realistic pricing.

3. The premium segment remains almost unaffected (0 to -3%). Buyers in this segment are not restricted by lending — they buy with a higher down payment (40-50%) or with cash. Between 2022-2025 in Western Europe we saw exactly this — while the average market adjusted by 10-15%, premium properties actually became more expensive.

4. Strengthening the effect of green discounts. If the standard interest rate rises to 4% and the discount for class A+ remains 0.50-0.75%, the difference between a "green" and a "standard" mortgage will become even more strategically important. Properties with energy class A/A+ will retain most of their value, while class EG properties will become illiquid assets.

The Bulgarian market has experienced interest rate hikes before. In 2008-2009, interest rates on new mortgages reached 8-91%, property prices fell by about 30-40% in the weakest areas. But this was against the backdrop of global financial crisis, a sharp rise in unemployment and a sudden halt in external capital flows.

The current situation is structurally different:

Interest rate hike to 3-4% It would NOT be fatal for the market. It would create:

If you take out a mortgage today for 2.46% and in 5 years the interest rate becomes 3.5%, you can:

The only scenario in which an interest rate rise would be fatal for the individual buyer is if he bought a property with a poor energy rating in an unsafe area at the edge of his means. This is the reason why this entire article even exists.

Interest rates change, regulations tighten, prices fluctuate — but there are three constant, structural forces that will fuel the demand for quality housing in Sofia and the major cities over the next 5-10 years. These are forces that are little talked about, but which make the difference between a market that falls and a market that simply slows down.

NSI data for 2024 shows a clear picture:

Plus Plovdiv, which for the first time in years has a positive mechanical growth of +2,318 people, and Burgas, which also draws population from all over the country.

The picture becomes even more dramatic when looking at the other side – the depopulated areas. The population of Vidin between the last two censuses decreased by 25% for 10 years. Smolyan is now under 24,000 people, and in small regional centers the demographic decline is accelerating. Currently Only a quarter of Bulgaria's population lives in villages — the remaining 75% are concentrated in cities, and 20.11% of the total population lives in Sofia (1.29 million people).

Why is this a structural force? Because of the economic gap. According to NSI data for Q4 2025, the average gross wage in Sofia (capital) is 3,745 leva (1,914 euros), while for the whole country it is 2,678 BGN (1,369 EUR) — a difference of almost 40%. The scissors open up even more dramatically towards the weakest regions: in Vidin the average salary is around 1,823 BGN. — more than 2 times lower than Sofia. With such a huge income gap, the flow of young people from the countryside to the capital will not stop. It is a function of economic reality, not a market cycle.

This is the phenomenon that is talked about the least, but which has the greatest effect on the quality property segment. According to NSI data for 2024:

The key feature of this segment — they are buyers, not renters. They have savings, they have income from abroad (many work remotely for existing employers), they have a relatively low dependence on Bulgarian mortgage financing (they pay with a 40-70% deductible or even in cash), and they are looking for quality, not cheap price.

There are several clear sub-profiles:

1. 90s throwbacks. People who emigrated in 1990-2005, who are now in their late 50s, have accumulated significant funds abroad and are returning to spend more peaceful years in Bulgaria, where they can have a better quality of life with less expenses. They buy ready-made class A properties in established areas, often outright in cash.

2. Young professionals after training. Graduates from London, Amsterdam, Berlin, Madrid who choose to return to Sofia or work remotely for a foreign employer with a salary of €4-8,000/month. They buy premium apartments in Lozenets, Iztok, Krastova Vada, Vitosha with a mortgage loan, but with a much higher deductible than the average.

3. Parents of children who remained abroad. Here's the interesting twist — children of immigrants often return before your parents, attracted by the tax breaks in Bulgaria (10% flat tax), more affordable education for their children, and a better quality of life.

This is the most underestimated power. According to official data from the Ministry of Labor and Social Policy:

And here's the key point - employers' organizations claim that Bulgaria's real need is 145,000 – 200,000 foreign workers per year. The government is already adopting measures to speed up the process — up to 50% of a company's staff can be foreigners, shorter deadlines, digitalized permits.

For comparison, in Romania, over 140,000 foreign workers from third countries were reported at the end of 2024, and 1.1 million foreigners (born abroad) live in Greece. Bulgaria's movement in this direction is inevitable.

What does this mean for the real estate market? Foreign workers they don't buy in bulk — they rent. But their growth creates huge demand on the rental market, especially in the peripheral neighborhoods of Sofia and in Varna and Burgas. This sets off a chain reaction:

When we combine the three forces:

| Strength | Annual growth |

|---|---|

| Internal migration (net) | +5,163 people |

| Bulgarians returning from abroad | +18,200 people |

| New foreign workers | +24 642 permits |

| Total annual demand | ~48,005 people |

Against this only 12,000-13,000 new homes per year are put into operation throughout the country. The mathematics is simple and uncompromising — structural deficit that will deepen.

There is one additional, more subtle change that is little talked about. In 2026, for the first time Bulgaria can become an attractive destination for institutional investors (funds buying homes in bulk for rental). There have been no formal obstacles so far, but the decisive factor is that Bulgaria is already in the European Banking Union — and this reduces the risk for such investors and makes portfolio purchases possible.

If this trend starts to take effect (and there are first signs), it will hit the middle segment and will add another layer of search, which the market has not yet taken into account.

Here the picture becomes clearer and more dramatic:

The difference between a class A property and a class E or F property will reach 40-60% in price per square meter by 2030. This is not a market fad, but a structural effect of:

We expect a massive wave of renovation of the old stock, driven by:

Owners who do NOT renovate will see their properties become unsaleable assets. Owners who DO renovate and move to Class B will see a jump in value of 25-40%.

The investment flow will be concentrated in:

After the initial normalization in 2026-2027, we expect:

The Bulgarian real estate market is undergoing the most significant structural change since the privatization of the 1990s. The combination of the eurozone, green regulations, and accumulating capital in banks is creating a window of opportunity that will not remain open for long.

If you are a buyer:

If you are a seller:

If you are an investor:

The Modern Home Bulgaria team monitors the banking and real estate market daily. If you are planning a purchase, sale or investment and need personalized advice to access the best financing conditions, contact us.

📞 For an individual property valuation, preliminary consultation with a banking partner, or investment strategy — book an appointment with our team at modernhomebulgaria.com/contacts